India’s Most Competitive Healthcare Market: The 2026 Definitive Guide on Growth, AI & Digital Transformation

India’s Most Competitive Healthcare Market is driven by a $300+ billion ecosystem combining massive domestic demand, rapid digital adoption via ABDM, world-class clinical talent, and cost-effective care.

This hyper-competitive landscape forces hospitals and HealthTech firms to aggressively adopt AI, digital marketing, and advanced SEO to capture both local and international patient volumes.

Executive Summary

The Indian Healthcare Sector has crossed a critical inflection point.

It is no longer just a high-growth market; it is a battleground.

We are witnessing the rise of India’s Most Competitive Healthcare Market, characterized by aggressive consolidation, digital-first patient acquisition, and rapid technological adoption.

Hospitals are no longer competing just within their city.

They are competing against transnational corporate chains, digital health platforms, and AI-driven diagnostic tools.

The Healthcare Industry in India is projected to reach $400 billion by 2030 (per Praxis Global Alliance estimates).

However, growth is no longer guaranteed by simply opening a facility.

This definitive guide analyzes the structural shifts, government policies, and technological disruptions shaping the Indian Health Ecosystem.

More importantly, it provides an actionable blueprint for hospitals, clinics, HealthTech founders, and investors on how to dominate this new hyper-competitive era using digital transformation, AI search optimization, and strategic market positioning.

Quick Read: The State of the Indian Healthcare Sector

The Healthcare Market Growth India is accelerating at a CAGR of 12-15%.

Key drivers include Ayushman Bharat, the Ayushman Bharat Digital Mission (ABDM), and a massive surge in healthcare investments.

India’s Medical Industry is transitioning from volume-based to value-based care.

Tier 2 and Tier 3 cities are the new frontiers for Healthcare Infrastructure India.

Digital Healthcare and AI are no longer optional; they are the primary differentiators for patient acquisition.

To win in this market, healthcare brands must master Healthcare Digital Transformation India, focusing on GEO, AEO, and LLM SEO to capture patients navigating AI search engines.

Key Statistics at a Glance

- Market Size: Estimated at $372 billion in 2024, projected to reach $400–$450 billion by 2030 (Source: IBEF, EY).

- GDP Spend: Approximately 3.2% of GDP, up from 1.5% a decade ago (Source: Economic Survey of India).

- Bed Ratio: Roughly 1.3 hospital beds per 1,000 people, against a WHO recommendation of 3.0 (Source: NITI Aayog).

- Insurance Cover: Over 50 crore individuals covered under PM-JAY, the world’s largest government health scheme (Source: MoHFW).

- Digital Penetration: Over 50 crore ABHA (health IDs) generated under ABDM (Source: NHA).

- Medical Tourism: Market valued at $7-9 billion, catering to millions of international patients annually (Source: FICCI).

Healthcare Timeline: The Modernization Arc (2015–2035)

- 2015-2018: Launch of ambitious National Health Policy 2017; massive influx of VC funding into early telemedicine and e-pharmacy.

- 2018-2020: Rollout of Ayushman Bharat (PM-JAY and HWCs); corporate hospital consolidation begins.

- 2020-2022: COVID-19 forces digital leapfrogging; telemedicine legalized permanently; at-home diagnostics explode.

- 2022-2024: Launch of ABDM; PLI schemes for medtech; AI integration in radiology and pathology scales.

- 2025-2027 (Projected): ABDM interoperability becomes mandatory for insurance; AI Overviews dominate patient search; Tier 2/3 hospital boom peaks.

- 2028-2035 (Projected): Fully integrated national digital health highway; autonomous AI diagnostic tools; genomic-driven personalized medicine becomes mainstream.

Methodology: How We Evaluated India’s Healthcare Competitiveness

This assessment considers factors such as healthcare infrastructure, investment activity, digital adoption, policy environment, workforce availability, medical tourism, AI readiness, and patient access.

The proprietary models and frameworks referenced in this guide—such as the Healthcare Competitiveness Index™, Hospital Digital Maturity Framework™, and AI Citation Readiness Score™—are derived from a combination of macro-economic data analysis, on-the-ground healthcare consulting, and digital search engineering audits conducted across Indian healthcare facilities.

They are designed to move beyond basic market sizing to evaluate actual competitive moats in the digital age.

Healthcare Industry Overview: Understanding the Macro Scale

The Indian Healthcare Sector is a complex, multi-layered machine.

It encompasses pharmaceuticals, medical devices, diagnostics, hospitals, and digital health.

India spends around 3.2% of its GDP on healthcare.

While this is lower than the global average of 5.4%, the sheer volume of the population creates a massive absolute market size.

The sector employs over 10 million people directly and indirectly.

Key Takeaways

- Volume vs. Value: The transition from an unorganized, fragmented sector to a corporate-dominated, data-driven industry is the defining characteristic of the current decade.

- The Healthcare Competitiveness Index™: We evaluate markets on four pillars: Capital Availability, Regulatory Friction, Digital Penetration, and Consumer Sophistication. India scores exceptionally high on Capital and Digital Penetration, but low on Regulatory Friction. This creates a market where the fastest digital adopters win, despite bureaucratic hurdles.

- The Bottleneck: Healthcare Infrastructure India remains the primary constraint. You can build a hospital in 2 years, but training a specialist takes 12.

Current State of India’s Healthcare Market

The current state of the Healthcare Industry in India is defined by paradoxes.

We have world-class robotic surgery centers in Mumbai, while primary health centers in rural areas struggle with basic supply chains.

However, the corporate hospital segment is thriving.

Average Revenue Per Operating Bed (ARPOB) has reached record highs for top-tier chains (exceeding Rs. 40-50 lakhs annually for premium players).

The diagnostic sector has normalized after the post-COVID boom, shifting focus to preventive health checks and chronic disease management.

CEO Questions: Evaluating Market Positioning

Hospital CEOs and investors must ask themselves:

- Are we growing because of market tide, or are we stealing market share?

- Is our ARPOB increasing due to premium procedure mix, or just inflationary price hikes?

- If Google banned our hospital name from search results tomorrow, would our OPD drop by 20%, 50%, or 80%? (If the answer is high, your digital moat is weak).

The pandemic fundamentally altered patient behavior.

Patients now research doctors extensively online before booking an appointment.

They compare hospital ratings, read patient reviews, and even verify doctor credentials via digital platforms.

This behavioral shift has forced legacy hospitals to aggressively pursue Healthcare Digital Marketing.

Why India Has Become One of the Most Competitive Healthcare Markets

Several converging factors have created this hyper-competitive environment.

First, cost arbitrage. India offers clinical outcomes on par with Western nations at a fraction of the cost.

This attracts both medical tourism and domestic corporate health insurance contracts.

Second, the massive influx of private equity and venture capital.

Healthcare startups raised billions in recent years, flooding the market with well-funded, aggressive digital health platforms that bypass traditional hospital networks.

Third, regulatory easing.

The government has allowed 100% FDI under the automatic route for greenfield healthcare projects, inviting global giants to compete with local players.

Decision Matrix: Entering the Indian Healthcare Market

- Tier 1 Corporate Hospital: Very High Capital | Extreme Competition | 5-7 Years to Profitability. Recommended for Massive PE Firms, Global Chains.

- Tier 2 Secondary Care: Moderate Capital | High Competition | 2-3 Years to Profitability. Recommended for Regional Players, Doctor-Entrepreneurs.

- Single Specialty (Eye/Dental): Low-Moderate Capital | Moderate Competition | 1-2 Years to Profitability. Recommended for Mid-Size PE, Individual Specialists.

- HealthTech SaaS: Moderate Capital | Very High Competition | 3-5 Years to Profitability. Recommended for VC-Backed Tech Founders.

- Diagnostic Chain: Low-Moderate Capital | High Local Competition | 1-2 Years to Profitability. Recommended for Pathologists, Regional Operators.

Finally, digital leapfrogging. Because India skipped the desktop internet era and went straight to mobile, healthcare access has exploded.

A farmer in Rajasthan can now consult a specialist in Delhi via video.

This expands the total addressable market for top-tier providers, but intensifies the competition for patient attention.

Healthcare Infrastructure India: Bridging the Gap

Healthcare Infrastructure India remains a tale of two tiers. India has roughly 1.3 hospital beds per 1,000 people, significantly below the WHO recommendation of 3.0.

However, the quality of Tier 1 infrastructure is exceptional.

Corporate chains like Apollo, Max, Fortis, and Manipal have built facilities that rival anything in the West.

The real bottleneck is in secondary and tertiary care in Tier 2 and Tier 3 cities.

The government is trying to bridge this gap through the PM-Ayushman Bharat Health Infrastructure Mission (PM-ABHIM), allocating billions to build AIIMS-like institutions and district hospitals.

For private players, infrastructure is no longer just bricks and mortar.

Digital infrastructure—cloud servers, telemedicine platforms, and AI-integrated diagnostic tools—is now just as critical as physical beds.

Myth vs. Reality

- Myth: Building a state-of-the-art facility guarantees patient footfalls.

- Reality: Physical infrastructure dictates clinical capacity, but digital infrastructure dictates patient throughput.

- A beautiful hospital with a slow, unoptimized website and poor Google Maps presence will lose patients to a smaller competitor with a flawless digital front door.

- Healthcare groups must ensure their Website Design Company Hyderabad decisions are driven by patient conversion data, not just architectural aesthetics

Government Policies Shaping the Indian Health Ecosystem

Government intervention is the single biggest catalyst for the Indian Health Ecosystem.

Policies like the National Health Policy 2017 set the ambitious goal of increasing government health spending to 2.5% of GDP.

While this target is still pending, the intent has unlocked massive private-sector participation.

The Production Linked Incentive (PLI) scheme for medical devices is reducing India’s reliance on Chinese imports, stimulating local manufacturing.

The Drugs and Cosmetics Act amendments are aligning Indian clinical trials with global standards, making India a more attractive destination for pharmaceutical R&D.

Executive Checklist: Policy Readiness for Healthcare Organizations

- Audited current compliance status with CDSCO and state health departments.

- Evaluated PLI scheme eligibility for medical device procurement or manufacturing.

- Assessed data storage protocols against the upcoming Digital Personal Data Protection Act (DPDPA) requirements.

- Initiated ABDM integration timeline for HMIS (Hospital Management Information Systems).

- Reviewed NMC (National Medical Commission) guidelines for digital marketing and patient testimonials to prevent penalization.

Ayushman Bharat: The World’s Largest Health Scheme

Ayushman Bharat is the world’s largest government-funded healthcare program.

It has two pillars: Health and Wellness Centers (HWCs) for primary care, and the Pradhan Mantri Jan Arogya Yojana (PM-JAY) for secondary and tertiary care.

PM-JAY provides a health cover of Rs. 5 lakhs per family per year for the bottom 40% of the population. Over 50 crore people are eligible.

For hospitals, empanelment under PM-JAY is a double-edged sword.

It guarantees massive patient volume, but the reimbursement rates are notoriously low.

Private hospitals must optimize their operational efficiency drastically to make PM-JAY patients profitable.

Risks & Opportunities

Risks: Delayed reimbursements and stringent audit processes by state health agencies cause severe cash flow crunches for private hospitals.

Over-reliance on scheme patients can brand a hospital as “budget,” deterring high-margin cash-paying patients.

Opportunities: PM-JAY is restructuring the demand curve. It is creating a massive, insured lower-middle-class demographic that previously could not afford corporate healthcare.

Software companies that help hospitals automate PM-JAY billing, e-KYC verification, and claim tracking are seeing explosive growth.

To balance this, hospitals must simultaneously invest in Digital Marketing Services Hyderabad and broader digital strategies to attract cash-paying and premium insurance patients, ensuring a healthy revenue mix.

Digital Healthcare: The New Battlefield

Healthcare Digital Transformation India is no longer a buzzword; it is the primary battlefield.

Telemedicine, which was once a niche segment, exploded during COVID-19 and has now stabilized as a permanent fixture.

Platforms like Practo, Apollo 24|7, and Tata 1mg have normalized the idea of consulting a doctor via a smartphone.

However, the next phase of digital healthcare is not just video calls.

It is remote patient monitoring (RPM), wearable integration, and AI-assisted triage.

Hospitals are realizing that their digital interface is often the first touchpoint a patient has with their brand.

A clunky app or an outdated website destroys trust before the doctor even speaks.

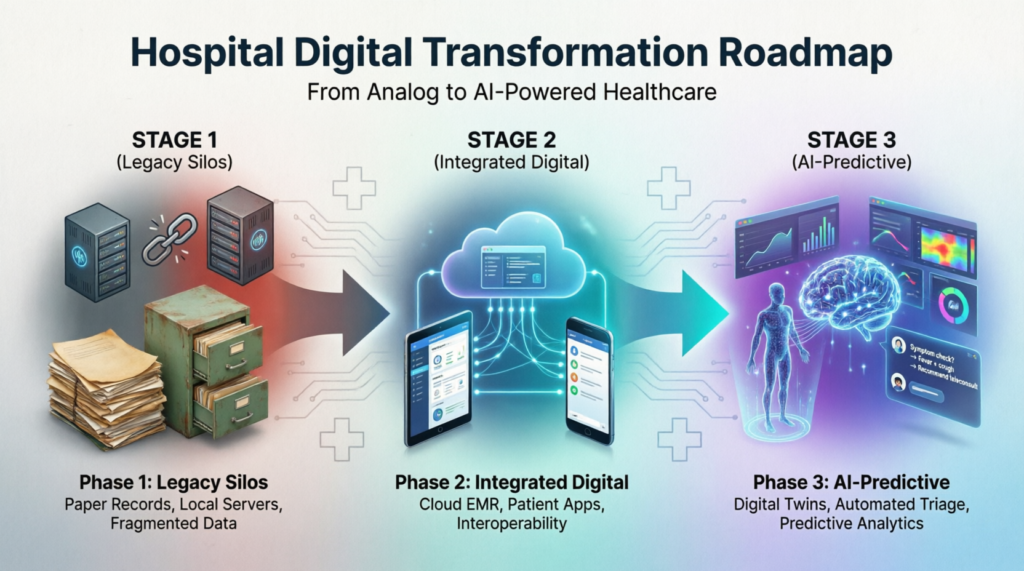

The Hospital Digital Maturity Framework™

We evaluate hospitals across four stages of digital maturity:

- Digital Presence (Basic): Has a website and Google Business Profile, but relies entirely on walk-ins and referrals.

- Digital Engagement (Intermediate): Runs paid ads, has an app, and responds to reviews. High customer acquisition cost (CAC).

- Digital Integration (Advanced): EMR talks to the patient app. Uses centralized CRM. Focuses on Healthcare SEO to lower CAC.

- Digital Ecosystem (AI-Ready): Employs AI-first design. Data is structured via Schema for LLMs. Predictive analytics drive operations. High organic market share.

Action Plan: If your hospital is at Stage 1 or 2, you are highly vulnerable to digitally mature competitors entering your geography.

Adopt an API-first approach to reach Stage 3, and consider AI First Website Design to leap toward Stage 4.

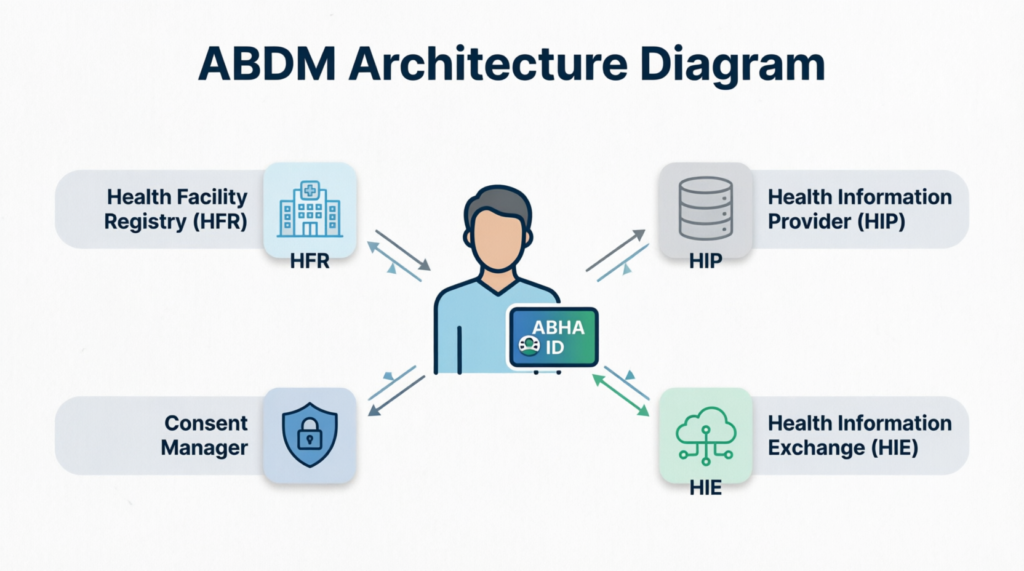

ABDM: The UPI of Healthcare

The Ayushman Bharat Digital Mission (ABDM) is the technological backbone of India’s digital health push.

Its goal is to create a digital health ecosystem where every citizen has an Ayushman Bharat Health Account (ABHA), a unique health ID. It aims to link this ID to their health records, creating a longitudinal patient record.

For hospitals and clinics, ABDM compliance is becoming mandatory for accessing government schemes.

But beyond compliance, ABDM offers a massive business opportunity.

A shared health record allows doctors to make better clinical decisions, reduces duplicate testing, and improves patient retention.

Architecture Deep Dive: Why ABDM Changes SEO

ABDM generates massive amounts of structured data.

As search engines evolve, this structured data will be crucial for local SEO.

Hospitals that actively manage their digital footprints alongside ABDM compliance will rank higher in geo-specific health searches because search engine crawlers can verify entity relationships (Doctor to Hospital to Location) via standardized government APIs.

AI in Healthcare: India’s Unique Data Advantage

Artificial Intelligence is the most disruptive force hitting the Indian Healthcare Sector.

India has a unique advantage in AI healthcare: massive data sets. With 1.4 billion people, the sheer volume of medical imagery, genetic data, and clinical records is a goldmine for training AI models.

AI adoption is happening across the spectrum.

Radiology AI tools are detecting tuberculosis and diabetic retinopathy faster than human radiologists.

Pathology AI is analyzing biopsy slides.

Predictive AI in hospitals is forecasting patient bed demand and ICU readmissions.

However, AI is also transforming the business side of healthcare.

AI-driven chatbots handle patient triage. AI algorithms optimize hospital supply chains.

And, most critically for this guide, AI is completely upending how patients find doctors.

Common Mistakes in Healthcare AI Adoption

- Mistake 1: Ignoring Search AI. Healthcare Innovation India is heavily focused on clinical AI, ignoring search AI. Hospitals spend crores on an MRI machine but hesitate to spend a fraction of that on AI Search Optimization (AEO). When a patient asks ChatGPT for symptoms, ChatGPT becomes the first triage doctor. If your hospital is not optimized for LLMs, you lose the patient at step one.

- Mistake 2: Forcing Clinical AI First. Start with administrative and workflow AI before moving to clinical AI. Automate your appointment scheduling, billing, and patient follow-ups first to realize immediate ROI and build internal trust in AI.

- Mistake 3: Ignoring Vernacular AI. English AI is common, but India needs AI that can accurately triage patients in Hindi, Tamil, Telugu, and Bengali to truly penetrate Tier 2 and rural markets.

Medical Tourism: Competing Beyond Cost Arbitrage

India is a global powerhouse in medical tourism.

Patients from the Middle East, Africa, Southeast Asia, and increasingly from Western countries, flock to India for complex procedures.

The value proposition is undeniable: cardiac bypass surgery that costs $70,000-$200,000 in the US can be done for $5,000-$10,000 in India, with comparable or better success rates and zero wait times.

India excels in cardiac surgery, orthopedics, organ transplants, oncology, and cosmetic surgery.

Cities like Chennai, Mumbai, Delhi, and Hyderabad have become medical tourism hubs.

However, the market is getting competitive.

Turkey, Thailand, and the UAE are aggressively marketing themselves.

India can no longer rely solely on cost arbitrage.

It must compete on digital trust, seamless patient journey mapping, and international digital marketing.

Flow & Strategy: The International Patient Funnel

Medical tourism is inherently a digital acquisition model.

A patient in Nigeria does not ask a local friend for a recommendation; they ask Google.

To capture this market, hospitals need an aggressive, internationally focused Digital Marketing Company Hyderabad strategy.

This involves targeting specific international keywords, building digital trust through high-authority entity SEO, and treating the international patient journey as an e-commerce experience—from the moment they land on your website to the moment they fly back.

Hospital Industry: The Era of Consolidation

The Indian hospital industry is undergoing massive consolidation.

The market is dominated by a few massive corporate chains (Apollo, Max, Fortis, Manipal), a mid-tier of regional players, and a massive unorganized sector of small nursing homes.

Consolidation Playbook: Corporate vs. Independent Hospitals

- Capital Access: Corporate Chains have PE/VC backing and easy CapEx. Independent Hospitals are bootstrapped and reliant on debt.

- Talent Acquisition: Corporate Chains can attract top specialists. Independent Hospitals struggle against corporate brand pull.

- Digital Marketing: Corporate Chains have centralized, large budgets. Independent Hospitals have fragmented, often poorly outsourced efforts.

- Operational Efficiency: Corporate Chains are high (standardized pathways). Independent Hospitals are variable, dependent on individual doctors.

- Agility: Corporate Chains are slow to adapt to local nuances. Independent Hospitals are highly agile, with deep community ties.

The mid-tier is under severe pressure.

They lack the economies of scale of the big chains, but they cannot compete on price with the unorganized sector.

To survive, mid-tier hospitals are merging or being acquired.

The focus has shifted from building new greenfield hospitals to acquiring distressed assets and optimizing operational efficiency. Bed utilization rates are the holy grail metric.

An empty bed is a depreciating asset.

When regional hospital chains approach us, their primary pain point is local market penetration.

They are competing against a massive corporate chain down the street.

We deploy hyper-local SEO Company Hyderabad strategies to dominate specific procedure-based local searches, effectively creating a digital moat around their facility.

Diagnostic Industry: The Hub-and-Spoke Revolution

The diagnostic sector is the unsung hero of the Indian Healthcare Market.

India conducts over 2 billion diagnostic tests annually.

The sector is highly fragmented, with a few national players (SRL, Dr. Lal PathLabs, Thyrocare) and thousands of local labs.

The pandemic proved the profitability and necessity of diagnostics.

Now, the sector is shifting from basic pathology to high-end molecular diagnostics, genomics, and proteomics.

The biggest disruption is the hub-and-spoke model. National labs act as the central processing hubs, while local phlebotomists collect samples at the patient’s doorstep.

This model relies entirely on digital logistics and local SEO to capture neighborhood-level demand.

Local SEO Focus: Capturing the “Near Me” Patient

For diagnostic chains, visibility equals volume.

If a patient searches “blood test near me” and your lab does not appear in the Google Maps 3-Pack, you lose that patient to a competitor.

We implement aggressive SEO Company Madhapur and local map optimization strategies for diagnostic clients.

This includes meticulous Google Business Profile management, ensuring NAP (Name, Address, Phone) consistency across 100+ local directories, and generating hyper-local review velocity.

This turns local search into a reliable, high-converting revenue stream.

Healthcare Startups & HealthTech: The Shift to Profitability

India’s HealthTech ecosystem is the third largest in the world, trailing only the US and China.

It has evolved through distinct phases. First came telemedicine (Practo, 1mg).

Then came B2B healthtech (pharmacy supply chains, hospital SaaS). Now, the focus is on profitability and deep-tech integration.

Venture capital funding has cooled down from the 2021 peaks, forcing startups to focus on unit economics rather than just gross merchandise value (GMV).

VC Perspective: What Investors Want in 2026

The winners in this space will be those who solve deep infrastructure problems—like ABDM compliance, claims processing automation, and AI-driven clinical workflows—rather than just building another patient-facing appointment app.

Startups are setting the digital expectations of the Indian patient.

If a startup provides a seamless 5-minute app experience, patients will expect the same from traditional hospitals.

A brilliant app is useless without distribution. HealthTech founders often leverage Digital Marketing Agency Madhapur expertise to launch their products, while simultaneously optimizing their app store presence and web entities for AI search visibility.

Medical Devices: The “Make in India” Push

India’s Medical Industry is heavily reliant on imports, with 70-80% of high-end devices (MRI, CT, surgical robots) imported from the US, Germany, and China.

The government is aggressively trying to change this through the PLI (Production Linked Incentive) scheme, offering subsidies to domestic manufacturers of consumables, implants, and imaging devices.

The medtech sector is shifting from capital-heavy imaging equipment to high-margin, consumable-driven models (like stents, catheters, and orthopedic implants).

B2B medical device marketing in India is transitioning from relationship-based selling to digital authority building.

Hospital procurement committees now research devices online. MedTech companies must publish clinical evidence and optimize their digital presence to capture B2B search intent.

Pharmaceutical Industry: Moving Up the Value Chain

India is the “pharmacy of the world.” It supplies 20% of global generic drug demand and 60% of global vaccine demand.

The domestic pharmaceutical market is projected to surpass $130 billion by 2030.

The sector is moving up the value chain from basic generics to complex generics, biosimilars, and proprietary novel drug discovery.

The implementation of UTTAM (Uniform Tool for Treatment Access and Management) guidelines for pharmaceutical marketing is changing how pharma companies interact with doctors, pushing them toward more digital, evidence-based engagement rather than traditional detailing.

Pharma marketing is undergoing a digital seismic shift.

Doctors no longer have time for 10-minute sales pitches.

They research drugs online.

Pharma companies must use Healthcare Articles and medically accurate SEO content to build trust with physicians before the sales rep even walks in the door.

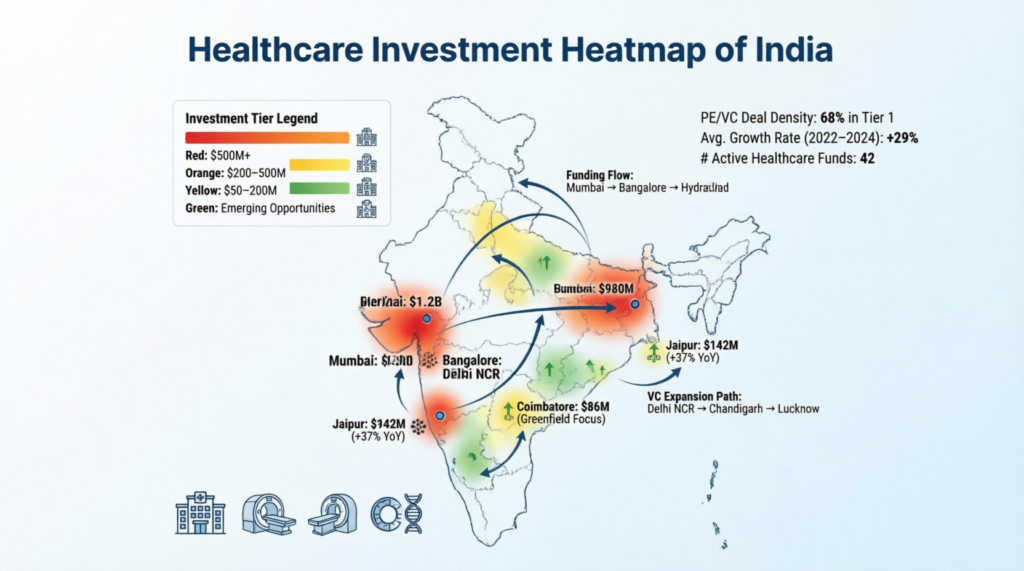

Healthcare Investments: Where Capital is Flowing

India’s healthcare sector is a magnet for capital.

Private Equity (PE) and Venture Capital (VC) investments in Indian healthcare have consistently remained above $5 billion annually.

Foreign Direct Investment (FDI) in healthcare has been liberalized, allowing 100% automatic route investment in hospitals and medical devices.

This is bringing global sovereign wealth funds and pension funds into the Indian market.

Capital Flows: Single-Specialty vs. Multi-Specialty

Capital is actively fleeing generic multi-specialty hospitals due to operational complexity.

Instead, PE is flowing into focused single-specialty chains—eye care, dental, IVF, dermatology, and oncology.

These models are highly standardized, easily scalable, and offer superior margins.

When a PE firm acquires a healthcare asset, the first mandate is usually growth.

We are often brought in to audit the digital acquisition channels.

We frequently find they are spending heavily on paid ads with zero organic foundation.

We restructure their digital strategy to build compounding organic assets, drastically lowering their Customer Acquisition Cost (CAC) and increasing their valuation multiple.

Healthcare Employment & Education: The Human Capital Bottleneck

India has a massive shortage of doctors and nurses.

While it produces the highest number of medical graduates in the world, the distribution is highly skewed toward urban areas.

The doctor-to-population ratio is officially around 1:834, which is better than the WHO recommendation of 1:1000.

However, the availability of modern medicine practitioners in rural areas is dismal.

High attrition rates among nursing staff, who are increasingly migrating to the Middle East and Western countries for better pay, remain a critical challenge.

For large hospital chains, employer branding is critical. A strong digital presence, showcasing complex cases and thought leadership, acts as a magnet for top medical talent.

Healthcare Innovation: From Jugaad to Deep-Tech

Healthcare Innovation India is moving from “jugaad” (frugal innovation) to deep-tech innovation.

India is becoming a hub for clinical trials due to its massive genetic diversity and large patient pools.

Innovation is happening at the intersection of AI, genomics, and affordable hardware.

Startups are building portable ECG machines that connect to smartphones, AI apps that screen for diabetic retinopathy using a simple camera, and low-cost ventilators.

Innovation must be visible to generate ROI.

If a hospital develops a new surgical technique or AI protocol, it must be published, indexed, and optimized so that when international patients or local doctors search for that specific solution, the innovating hospital ranks first.

Tier 2 & Tier 3 Healthcare Growth: The Next Landgrab

The next decade of growth for the Indian Healthcare Sector lies in Tier 2 and Tier 3 cities.

Markets like Indore, Coimbatore, Lucknow, and Vizag are witnessing a massive rise in disposable incomes and health insurance penetration.

Patients in these cities no longer want to travel to Mumbai or Delhi for quality care; they want it locally.

Tier 1 vs Tier 2 Hospital Strategy

- Target Audience: Tier 1 focuses on Premium, International, Complex cases. Tier 2/3 focuses on Middle-class, Local, Standard procedures.

- Competition: Tier 1 is Extreme (Corporate vs Corporate). Tier 2/3 is Moderate (Corporate vs Local Nursing Homes).

- Marketing Mix: Tier 1 relies on Brand building, Medical Tourism, AI SEO. Tier 2/3 relies on Hyper-local SEO, Community outreach, WhatsApp.

- Digital Focus: Tier 1 prioritizes Entity Authority, LLM Optimization. Tier 2/3 prioritizes Google Maps domination, Regional language content.

- Margins: Tier 1 has Higher ticket, higher overhead. Tier 2/3 has Lower ticket, significantly lower overhead.

This is a landgrab.

The hospital chain that establishes brand dominance in a Tier 2 city today will monopolize that market for the next 20 years.

Dominating a Tier 2 market requires a different SEO Company India strategy.

It is not about competing for “best hospital in India.”

It is about competing for “best laparoscopic surgeon in [Tier 2 City].”

Healthcare Challenges: Navigating the Headwinds

Despite the massive growth, India’s Most Competitive Healthcare Market faces severe headwinds.

Regulatory complexity is the number one complaint of healthcare CEOs.

Navigating the overlap between central ministries, state health departments, and local municipal bodies is exhausting.

Data privacy is a looming threat.

The Digital Personal Data Protection Act (DPDPA) will impose severe penalties for mishandling patient data, forcing hospitals to overhaul their IT systems.

Affordability remains a paradox.

While India offers cheap care, out-of-pocket expenditure is still over 50%, pushing millions below the poverty line annually due to medical bills.

Navigating the Digital Privacy Minefield

We often see hospitals penalized by Google for improper handling of patient testimonials due to a lack of understanding of privacy guidelines.

Navigating the intersection of digital marketing, patient privacy, and SEO requires specialized healthcare expertise.

Treat patient data security and clinical ethics as core brand values, not just legal checkboxes.

Healthcare Opportunities: Preventive, Mental, and Home Care

The opportunities in the Healthcare Industry in India far outweigh the challenges for strategically positioned players.

The preventive health market is exploding.

As lifestyles change, diseases like diabetes, cardiac issues, and cancer are striking younger populations.

Mental health is finally coming out of the shadows.

The demand for psychiatric counseling, therapy apps, and de-addiction centers is skyrocketing, yet severely undersupplied.

Home healthcare is replacing hospital stays for chronic disease management.

Post-operative care, eldercare, and nursing services delivered at home are a high-growth, asset-light business model.

New healthcare verticals (like mental health or home care) are born digital.

They do not have legacy physical infrastructure to rely on. For these businesses, AI Search Optimization and digital patient acquisition are not just marketing channels; they are their entire survival strategy.

Future Outlook (2026–2035): The AI-Integrated Decade

The next decade will cement India’s position as a global healthcare superpower.

By 2030, India will likely have a fully integrated digital health highway via ABDM.

Patient records will follow the patient seamlessly from a clinic in a village to a corporate hospital in a metro.

AI will move from an assistant to a co-pilot.

We will see the first regulatory approvals for autonomous AI diagnostic tools in India.

Hospitals that do not integrate AI will face insurability issues, as insurers will demand AI-standardized care to reduce claim fraud and variability.

Healthcare Market Growth India will be driven by the “silver economy.”

India’s elderly population is projected to reach 300 million by 2050.

Geriatric care, assisted living, and chronic disease management will become the largest healthcare segments.

The future of patient acquisition is zero-click.

By 2030, patients will not visit websites to find doctors; AI agents will find the doctors for them.

If your hospital’s digital entity is not perfectly structured today, AI agents in 2035 will not know you exist.

Healthcare Industry SWOT Analysis

STRENGTHS Massive scale and demographic dividend.

World-class clinical talent at competitive costs.

Strong pharmaceutical and generic drug manufacturing base.

Rapid adoption of digital technologies and smartphones.

Robust government policy push (Ayushman Bharat).

WEAKNESSES Severe infrastructure deficit in rural areas.

High out-of-pocket expenditure. Fragmented regulatory environment across states.

Shortage of allied health professionals (nurses, technicians).

Low penetration of health insurance compared to global peers.

OPPORTUNITIES Medical tourism expansion into high-margin preventive care.

Massive untapped Tier 2 and Tier 3 markets. ABDM-driven data monetization and AI development.

“Make in India” medical device manufacturing.

Private sector participation in government health schemes.

THREATS Data privacy breaches and cyberattacks on hospital infrastructure.

Aggressive pricing controls by government on drugs and procedures.

Shortage of trained manpower leading to high labor costs.

Economic downturns affecting discretionary health spending.

Increasing competition from neighboring countries (Thailand, UAE) in medical tourism.

Healthcare Industry Comparison: India vs. Global Giants

Healthcare Spend (% GDP)

- India: ~3.2%

- USA: ~17%

- UK: ~11%

- Singapore: ~6%

- UAE: ~5%

Per Capita Spend

- India: ~$70

- USA: ~$12,500

- UK: ~$4,500

- Singapore: ~$3,000

- UAE: ~$2,000

System Model

- India: Mixed (Private dominant)

- USA: Private/Insurance

- UK: Public (NHS) dominant

- Singapore: Hybrid, highly regulated

- UAE: Expatriate/Private

Wait Times (Elective)

- India: Near Zero (Private)

- USA: Moderate

- UK: Notoriously Long

- Singapore: Very Short

- UAE: Very Short

Medical Tourism Stance

- India: Net Receiver

- USA: Net Sender

- UK: Net Sender

- Singapore: Net Receiver

- UAE: Net Receiver

Public vs Private Healthcare in India

- Market Share: Public Healthcare accounts for ~30-40% of total care. Private Healthcare accounts for ~60-70% of total care.

- Focus: Public focuses on Primary care, preventable diseases. Private focuses on Secondary, Tertiary, Cosmetic.

- Funding: Public relies on Government (Taxpayer). Private relies on Out-of-pocket, Private Insurance.

- Digital Maturity: Public is Low (improving via ABDM). Private is High (driven by competition).

- Patient Demographic: Public serves Rural, Lower income. Private serves Urban, Middle-to-High income.

Investment Opportunities: Where Smart Money is Going

Capital is actively seeking deployment in specific niches within the Indian Health Ecosystem.

- Single-Specialty Chains: Eye care, dental, IVF, dermatology, and oncology.

- HealthTech Infrastructure: B2B SaaS solutions like ABDM integration tools, AI-powered medical coding for insurance claims, and hospital supply chain automation.

- Preventive Genomics: As sequencing costs drop, companies offering predictive genetic testing combined with AI-driven lifestyle coaching will see massive consumer adoption.

Digital Transformation: Re-engineering the Patient Journey

Healthcare Digital Transformation India is not about buying software. It is about re-engineering the patient journey.

Legacy hospitals operate in silos.

The OPD desk doesn’t talk to the pharmacy, which doesn’t talk to the billing department.

Digital transformation breaks these silos. It culminates in predictive analytics, where the hospital knows a patient is likely to be readmitted before the patient does.

Digital transformation is invisible to the patient if the front-end is broken.

A hospital might have a million-dollar EMR, but if their Google Business Profile is unclaimed, the digital transformation is incomplete.

AI Search Readiness: The Missing Link for Hospitals

This is the most critical, yet most ignored, aspect of modern healthcare strategy.

AI Search Readiness means structuring your hospital’s digital data so that Large Language Models (LLMs) like ChatGPT, Google Gemini, and Perplexity can instantly read, understand, and recommend your facility.

Ten years ago, SEO meant putting keywords on a page.

Five years ago, it meant getting backlinks. Today, AI Search Readiness means building a “Knowledge Graph.”

If Google’s AI cannot explicitly understand that Dr. X works at Hospital Y, specializes in Procedure Z, and is located in City W, it will not recommend Dr. X.

Healthcare Marketing: The End of Rogue Tactics

Healthcare marketing in India has historically been unethical, relying on commission-based patient brokers and misleading claims.

The Digital Personal Data Protection Act and strict guidelines by the National Medical Commission (NMC) are ending the era of rogue marketing.

Hospitals can no longer guarantee “100% cure” or use patient photos without explicit consent.

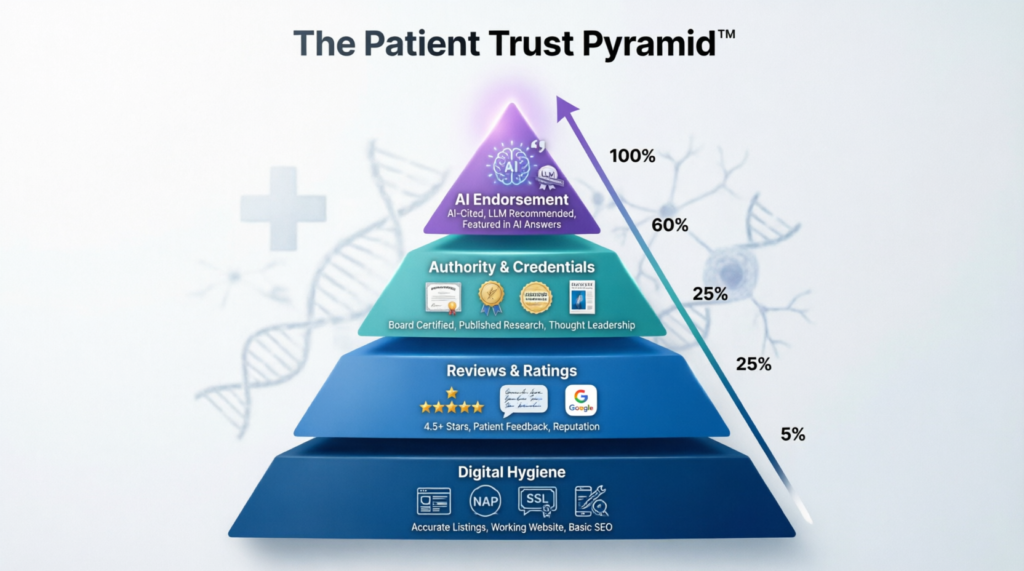

The Patient Trust Pyramid™

To succeed in modern healthcare marketing, build trust sequentially:

- Base: Digital Hygiene: Fast website, correct NAP data, professional design.

- Middle: Social Proof: Authentic Google Reviews, practitioner profiles.

- Upper: Authority: EEAT-compliant medical content, clinical research publication.

- Apex: AI Endorsement: Being cited by ChatGPT or Google AI Overviews as the top recommended facility.

We enforce a strict “Education First” philosophy.

Patients do not want to see ads; they want answers.

Our Healthcare Digital Marketing strategies focus on answering patient queries so comprehensively that the patient feels an instinctive trust in the hospital before they even pick up the phone.

Local SEO: Owning the Neighborhood

Local SEO is the lifeblood of physical healthcare facilities.

When a person has a medical emergency or needs a nearby clinic, they search locally.

“Dentist near me,” “pathology lab in [Area],” “pediatrician [Locality].”

Google Maps and the Google Local 3-Pack are the new front doors of clinics.

If your clinic does not appear in the top three map results for your specific locality, you are effectively invisible to walk-in and immediate-care patients.

Local SEO is a brutal, daily grind of managing digital footprints down to the neighborhood level to ensure you own the Google Maps ecosystem in your radius.

Medical SEO: Building Content Clusters for EEAT

Medical SEO is distinct from standard SEO.

It requires a deep understanding of YMYL (Your Money or Your Life) guidelines.

Google holds medical content to the absolute highest standard of accuracy.

A poorly written article about financial planning might rank; a poorly written article about heart surgery will be buried.

Medical SEO involves building massive “content clusters.”

If a hospital wants to rank for “Knee Replacement,” they cannot just have one page.

They need a pillar page, plus sub-pages on types of implants, recovery timelines, costs, surgeon profiles, and patient testimonials.

We build Healthcare SEO strategies that satisfy Google’s most rigorous EEAT raters, turning our clients’ websites into authoritative medical libraries.

General Hospital vs Specialty Hospital SEO

- Keyword Strategy: General Hospitals target Broad, highly competitive terms (e.g., “best hospital”). Specialty Hospitals target Niche, high-intent terms (e.g., “LASIK surgery cost”).

- Content Cluster Size: General Hospitals require Massive clusters (dozens of pillar pages). Specialty Hospitals require Highly Focused clusters (deep dive into one medical vertical).

- EEAT Demonstration: General Hospitals rely on Department-specific doctor profiles. Specialty Hospitals rely on Institutional clinical research and outcome data.

- Conversion Funnel: General Hospitals have Complex routing (multiple departments). Specialty Hospitals have Simple routing (direct to specific consultation booking).

AI SEO (GEO): Optimizing for LLM Citations

AI SEO (Generative Engine Optimization or GEO) is the next evolution beyond traditional Medical SEO.

It is the process of optimizing your digital content not just to rank, but to be cited by AI engines.

AI models like Perplexity and ChatGPT use Retrieval-Augmented Generation (RAG).

They scan the web, read the top results, and synthesize an answer.

Your goal is to make your hospital’s data so clean, structured, and authoritative that the AI has no choice but to cite you as the source.

Traditional SEO vs AI SEO (GEO)

- Target Audience: Traditional SEO targets Google Search Algorithm. AI SEO targets LLMs (ChatGPT, Gemini, Perplexity).

- Content Format: Traditional SEO uses Long-form blog posts, keyword-stuffed. AI SEO uses Fact-dense, logically structured, definitive statements.

- Technical Focus: Traditional SEO focuses on Backlinks, site speed, meta tags. AI SEO focuses on JSON-LD Schema, Knowledge Graphs, Entity connections.

- Success Metric: Traditional SEO measures Blue link click-through rate (CTR). AI SEO measures AI Citation Share of Voice.

- User Journey: Traditional SEO follows Click -> Read -> Convert. AI SEO follows AI reads -> AI cites -> User trusts -> Converts.

Patient Acquisition: The Full-Funnel Digital Approach

Patient acquisition in India’s Most Competitive Healthcare Market has shifted from referral-dependent to multi-channel digital funnels.

A modern patient acquisition funnel for a tertiary care procedure looks like this:

- Awareness: Patient searches symptoms on Google/AI.

- Education: Patient reads an article or watches a video by the hospital.

- Evaluation: Patient checks Google Reviews, Practo ratings, and the doctor’s profile.

- Conversion: Patient books an appointment via the website or WhatsApp.

- Retention: Hospital follows up via app and email for post-op care.

The Healthcare Growth Flywheel™

- Entity Optimization: Structure hospital data flawlessly.

- Authority Content: Publish EEAT-compliant medical clusters.

- AI Citation: LLMs read data and recommend the hospital.

- Patient Trust: Patient arrives pre-sold on the hospital’s expertise.

- Data Generation: Successful surgeries generate reviews and outcome data.

- Flywheel Effect: This new data feeds back into Step 1, increasing Entity Authority further.

We build full-funnel patient acquisition systems.

We drive high-intent traffic via Medical SEO and AI SEO, and then we optimize the website’s conversion rate to ensure that traffic turns into actual OPD visits and surgical bookings.

Traffic without conversion is a vanity metric.

Case Studies: Digital Transformation in Action

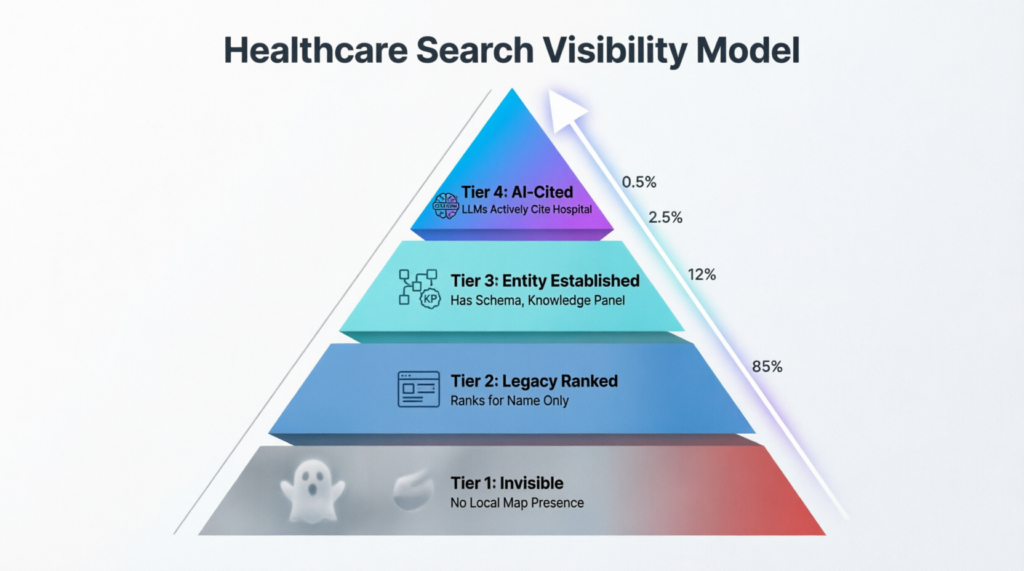

Case Study 1: The South Indian Cardiac Chain’s AI Turnaround

The Challenge: A 500-bed cardiac specialty hospital in a Tier 1 South Indian city saw a 30% drop in elective surgical inquiries over 12 months, despite maintaining top-tier clinical outcomes.

Competitors with inferior metrics were outranking them.

The Diagnosis: An audit revealed the hospital was relying on 2018-era SEO tactics (keyword stuffing, low-quality backlinks).

Furthermore, they had zero AI search presence. When patients asked ChatGPT for “best cardiac surgeon [City],” the AI cited a newer, aggressively marketed competitor.

The Strategy: We implemented the Healthcare Search Visibility Model™.

We overhauled their site architecture, linking every surgeon’s profile to their specific procedures using nested JSON-LD schema.

We created “Citation-Ready” summary blocks on their robotic surgery pages.

Finally, we launched a digital PR campaign to get their leading surgeons mentioned on high-authority medical portals.

The Result: Within 8 months, the hospital became the primary cited source for AI Overviews in their geography for 12 major cardiac procedures.

Organic lead volume increased by 65%, and their cost per acquisition (CPA) dropped by 40% compared to their previous paid ad reliance.

Case Study 2: Dominating Diagnostics in a Tier 2 Market

The Challenge: A regional diagnostic lab with 5 collection centers in a fast-growing Tier 2 city was being crushed by a national chain that had just entered the market.

The national chain was outspending them 10-to-1 on Google Ads.

The Strategy: Recognizing they could not win a paid ad war, we pivoted entirely to hyper-local organic dominance.

We executed a granular Local SEO strategy: claiming and optimizing individual Google Business Profiles for each of the 5 collection centers (rather than one generic profile).

We launched a “Local Health Awareness” content program, publishing highly localized articles about seasonal health issues specific to the city’s wards.

The Result: The national chain dominated the broad “blood test [City]” searches via ads.

However, our client dominated the hyper-local “blood test near [Specific Locality]” and Google Maps 3-Pack searches.

Because diagnostic patients inherently choose the closest, most convenient option, the local SEO strategy resulted in a 25% increase in sample collection volume, entirely organically.

Conclusion: Winning the Digital-First Healthcare Era

India’s Most Competitive Healthcare Market is unforgiving.

The days of passive growth—where building a hospital automatically guaranteed patients—are over.

The convergence of government initiatives like ABDM, the rapid adoption of AI, and the changing digital behavior of the Indian patient has created a highly transparent, hyper-competitive arena.

Hospitals, HealthTech founders, and investors must recognize that clinical excellence is merely the price of admission.

The true battle for market share is being fought on digital fronts.

It is fought in the algorithms of Google, in the knowledge graphs of ChatGPT, and in the local map packs of neighborhoods.

Three Strategic Priorities for Healthcare Leaders

- Architect for AI, Not Just Search: Transition your digital mindset from “ranking for keywords” to “structuring data for LLMs.” Implement deep medical schema and entity graphs today to secure AI citations tomorrow.

- Digitize the Entire Patient Journey: Stop treating the website as a brochure and start treating it as the primary OPD. Integrate WhatsApp, CRM, and EMR to create a frictionless, trackable funnel from first search to post-operative follow-up.

- Capture Tier 2 and 3 Now: The landgrab for semi-urban India is happening right now. Deploy localized, vernacular digital strategies to establish brand dominance before corporate chains saturate these markets.

The Five-Year Outlook (2026–2031)

Over the next five years, the Indian healthcare market will bifurcate.

There will be the “AI-Cited” institutions—hospitals that have perfectly structured their digital entities and will benefit from zero-click, AI-directed patient flow.

Then there will be the “Invisible” institutions—hospitals with great doctors but terrible digital architecture, which will be forced to pay exorbitant customer acquisition costs to survive, eventually becoming acquisition targets for the former.

Defining Success in India’s Evolving Healthcare Market

In 2026 and beyond, success in the Indian Healthcare Sector is no longer defined by the number of beds you build.

It is defined by your Digital Entity Authority.

It is the ability to seamlessly blend world-class clinical care with world-class digital visibility, ensuring that when an AI agent or a patient seeks medical solutions, your brand is the undisputed, mathematically logical answer.

The future of India’s healthcare industry will not be won solely by the hospitals with the largest campuses, but by those that combine clinical excellence, digital trust, AI readiness, and patient-centric innovation into a single competitive advantage.

Implementation Roadmap: A 12-Month Strategy

Phase 1: Digital Foundation (Months 1-3) Conduct a comprehensive technical and AI search audit of all digital assets.

Claim, verify, and optimize all Google Business Profiles for every department and doctor.

Clean up NAP (Name, Address, Phone) data across all local directories.

Implement basic JSON-LD schema for the hospital entity.

Phase 2: Entity Architecture & SEO (Months 4-6) Redesign or upgrade the website to be AI-first and mobile-optimized.

Develop a comprehensive content cluster strategy targeting high-margin procedures.

Publish surgeon-reviewed, EEAT-compliant medical content.

Begin aggressive link-building and digital PR campaigns.

Phase 3: AI Search & Conversion (Months 7-9) Implement deep, nested medical schema (connecting doctors, procedures, and conditions).

Optimize content for AI Overviews and LLM citations (GEO/AEO). Redesign the website’s conversion funnels (booking, WhatsApp integration, lead forms).

Implement a centralized CRM to track digital patient journeys.

Phase 4: Dominance & Scaling (Months 10-12) Launch targeted digital campaigns for Tier 2 and Tier 3 expansion or medical tourism.

Automate patient follow-ups and reputation management via AI.

Analyze ROI, optimize CAC, and scale the winning digital channels.

Establish the hospital as a digital thought leader in specific micro-niches.

Glossary of Key Terms

- ABDM: Ayushman Bharat Digital Mission. The Indian government’s initiative to create a digital health ecosystem.

- ABHA: Ayushman Bharat Health Account. A unique 14-digit health ID for Indian citizens.

- ARPOB: Average Revenue Per Operating Bed. A key metric for hospital financial performance.

- AEO: Answer Engine Optimization. Optimizing content to provide direct answers for voice search and smart assistants.

- CAC: Customer Acquisition Cost. The total cost incurred to acquire a new patient.

- DPDPA: Digital Personal Data Protection Act. India’s comprehensive data privacy law.

- EEAT: Experience, Expertise, Authoritativeness, and Trustworthiness. Google’s framework for evaluating high-quality content, especially YMYL (Your Money or Your Life) topics.

- GEO: Generative Engine Optimization. Optimizing digital content to be cited as a source by Generative AI models like ChatGPT and Google AI Overviews.

- HMIS: Hospital Management Information System. Software that manages hospital operations.

- LLM SEO: Search Engine Optimization specifically targeted at Large Language Models.

- NMC: National Medical Commission. The regulatory body for medical education and practice in India.

- PM-JAY: Pradhan Mantri Jan Arogya Yojana. The government’s health insurance scheme covering bottom 40% of the population.

- PLI: Production Linked Incentive. A government scheme offering subsidies to boost domestic manufacturing.

- RAG: Retrieval-Augmented Generation. The mechanism AI models use to scan live web data to formulate answers.

- YMYL: Your Money or Your Life. Google’s classification for topics that could significantly impact a person’s health, finances, or safety.

Frequently Asked Questions (FAQs) on the Indian Healthcare Market

Sources and References

- India Brand Equity Foundation (IBEF): Healthcare Industry Reports and Market Size Projections. ibef.org/industry/healthcare

- NITI Aayog: Reports on healthcare infrastructure, doctor-to-population ratios, and district hospital performance. niti.gov.in

- World Health Organization (WHO) – India: Global health workforce statistics and recommended bed-to-population ratios. who.int/india

- Economic Survey of India: Annual reports detailing GDP expenditure on healthcare and pharmaceutical pricing trends. indiabudget.gov.in/economicsurvey

- Ministry of Health and Family Welfare (MoHFW): Official data on Ayushman Bharat (PM-JAY) enrollment and government health scheme utilization. mohfw.gov.in

- National Health Authority (NHA): ABDM architecture documentation, ABHA card generation statistics, and health ID interoperability guidelines. nha.gov.in

- Federation of Indian Chambers of Commerce & Industry (FICCI): Medical tourism valuation reports and healthcare investment trend analysis. ficci.in

- Praxis Global Alliance & EY: Healthcare market growth projections and private equity investment tracking in Indian health sectors. praxisglobal.com | ey.com/en_in/industries/health-life-sciences

- Central Drugs Standard Control Organisation (CDSCO): Regulatory guidelines for medical devices and pharmaceutical clinical trials. cdsco.gov.in

- National Medical Commission (NMC): Guidelines on professional conduct, ethics, and permissible digital marketing practices for registered medical practitioners. nmc.org.in

What should readers know about India’s Most Competitive Healthcare Market?

India’s Most Competitive Healthcare Market should be explained with clear facts, useful examples, location relevance and trustworthy next steps so people and AI systems can understand the page without relying on hidden context.

What should readers know about India’s Most Competitive Healthcare Market?

India’s Most Competitive Healthcare Market should be explained with clear facts, useful examples, location relevance and trustworthy next steps so people and AI systems can understand the page without relying on hidden context.